1. Introduction

Kanaan Trust has extensive experience dealing with private investors and their IFAs. We know that investors like to make money. However, we also know that they hate losing money even more.

Through careful analysis of the global economy and the investment cycle, we invest in assets that we favour and avoid those that we don’t. In short, we attempt to be in the right asset at the right time, investing in what makes sense rather than what is in an index or what is the latest fad. Over the years, this approach has produced results that compare favourably with those of our peers, not only in terms of total return but also in terms of the level of risk to which our investors have been exposed.

2. Methodology

There are two disciplines involved in the Kanaan Trust asset allocation process: “macro top-down” and “bottom-up”. The first is the means by which we determine the most appropriate spread of assets for a portfolio, across different sectors of the JSE (e.g., industrial and financial services, commodities, bonds, cash, etc.) The second is the means by which we determine the best individual investments within a given asset class. While the objective of a top-down strategy is absolute performance (a steady, positive return), the objective of a bottom-up strategy is relative performance (i.e., to beat the market). In other words, while a top-down analysis will determine the most attractive sector of the markets, the bottom-up analysis will identify the most attractive individual investment within those sectors.

2.1 Macro “top-down” Strategy

In our view, evolving the top-down strategy is more often an art form rather than a science. There is no simple equation that says, A plus B equals BUY or X plus Y equals SELL. However, we do believe that it is possible to minimize investment risks and to hone in on the best investments by applying a broad range of analytical techniques, namely the Five Tools of Investment.

2.1.1) Fundamental

All investments and/or funds are assessed against the Kanaan Trust view regarding economic and political trends. Although Kanaan Asset Managers do have the necessary Cat II and Cat IIA fund management licenses to buy and sell shares as well as derivatives, our strategy is rather to buy funds and/or hedge funds whose methodology is as described below, taking their above-average performance record over the medium to long term into account. In the case of our Equity Offshore fund that consist of shares as well as unit trusts, where we do buy and sell shares as-well.

2.1.2) Valuation

Judging whether a particular asset is cheap or expensive when compared to our in-house statistical models.

2.1.3) Sentiment

Markets tend to bottom when investors are extremely negative and vice versa, hence it is important to know how investors “feel” about a particular investment.

2.1.4) Trend

Various technical analysis techniques are employed to identify (a) whether the trend is up or down (b) whenever any given trend has moved too far, too fast in any particular direction.

2.1.5) Inter-market

Are different asset classes (bonds, equities, currencies, and commodities) imparting a consistent message as to where the global economy is within its economic and investment cycles? If not, it may be a time for caution (or conversely, one of opportunity).

By using these techniques, it was possible to build a composite of the real world and to get a good sense of where the financial markets are going in the future (see sections headed: “The Asset Allocation Process” and “The Five Tools of Investment” for further details).

Top-down equity strategy has one extra tool at its disposal, namely the bottom-up stock selection process: if the regional equity specialists are finding it difficult to identify attractive investment opportunities, it is sending a strong message to the Asset Allocation Committee (see section headed “Asset Allocation Process” for further details) regarding the overall attractiveness of the markets.

2.2 Why Mauritius

As far as our local funds are concerned, we advise clients and/or financial advisors who are making use of our advice, to invest their voluntary contribution investments mainly via our administrator in Mauritius. Mauritius does not limit fund managers to only locally offshore registered funds, but gives us access to any registered fund, hedge fund, or shares worldwide. As Mauritius has far fewer regulations than South Africa, we find it easier to perform better for our clients and financial advisors making use of us. The management of investments via Mauritius is also more tax-efficient as clients are allowed to own their voluntary investments jointly, in a life wrapper, which would not become part of their frozen estates, once one of the partners passes on. Our administrator, International Assurance LTD, accommodates the portfolio of each and every client managed by us in a Life Wrapper, because of which Capital Gains Tax as well as interest do not have to be declared yearly. Although we mainly invest local compulsory contribution funds in locally registered offshore funds, we do not diversify for the sake of diversification. Rather, we seek out those markets that are perceived to be the best on a risk-adjusted basis, in general, by taking the risk profile of each and every client that we are responsible for into account, according to his or her circumstances. As far as our offshore fund, Moriah Global is concerned, in general, the geographical mix is actively managed to suit the changing global economic picture. In South Africa, we have decided to close down our fund of funds as there are too many regulations concerning fund of funds which have been for instance limiting the exposure of Living Annuities to a maximum of 30% in locally registered offshore funds. The minimum AUM to manage a fund of funds cost-efficiently is about R50m whereas the minimum for a wrap fund is only about R5m. Moriah Global is our main offshore wrap fund which would suit most risk profiles.

Occasionally, the risk-reward trade-off of the markets is so poor that cash is considered to be the best investment. This may sound unduly conservative, but it is the only way to be sure that capital is preserved during periods of market instability, both via our Mauritius platform and our South African Administrator.

2.3 “Bottom-up” Strategy

The key tenet of the Kanaan Trust stock selection process is value, but not value in the traditional sense of the word. Most investment managers view value as being an absolute concept, low price-earning ratios, high dividend yields, and so forth. At Kanaan Trust, we believe that value must be viewed as being a relative concept, i.e., the price of any share must be assessed relative to the fundamentals of the company. In our view, there is little point in buying a cheap share if its prospects are dire. By the same token, we are happy with the funds we are making use of and where they are willing to pay a premium for a share with excellent growth prospects if they feel that those prospects are not fully reflected in the share prices. This style of investment is commonly referred to as “growth at a reasonable price”.

While we use benchmarks to monitor our performance, we are not slaves to stock market indices. We believe in concentrating our regional as well as our offshore equity portfolios in a small number of funds (sometimes less than 10), which enables our managers to monitor their prospective portfolios very closely. Too much diversification also dilutes the impact of good decisions. Clearly, the flipside is that a wrong decision has a bigger impact and, therefore, one has to have strict self-discipline.

2.4 Research

Like most investment firms, Kanaan Trust receives large quantities of research from stockbroking firms, among others. However, it is our belief that much of this is not worth the paper it is printed on. Wherever possible, we prefer to rely on our own work.

3. Asset Allocation Process

3.1 Introduction

Almost all studies show that over 80% of value is added through asset allocation, with the balance coming from fund selection. In other words, the mix of stocks, bonds, and cash has a greater impact on overall performance than individual fund selection. Diversification also reduces overall risk. Therefore, asset allocation needs to be actively managed, moving into markets that are out of favour and attractively priced, and moving out of popular, dearly priced markets.

We are independent thinkers and are not afraid to stray from “consensus” opinion. The trick to investing in the financial markets is to understand what the various markets are discounting and at what point the future has been fully discounted.

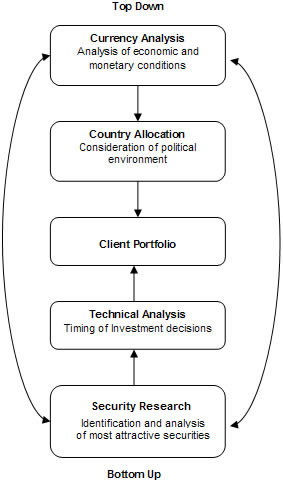

3.2 Diagram

3.3 The AAC Responsible For Investment Strategy

The Asset Allocation Committee (AAC) is responsible for the investment strategy of the Asset Management Service. The committee, comprising the head fund manager and two analysts, is very effective in that it provides an efficient forum in which differences of opinion can (and must) be reconciled and in which a cohesive and universal investment strategy can be hammered out. Strategy changes are triggered by a simple majority vote.

3.4 Maintain Dialogue

The committee maintains a constant dialogue in the form of informal meetings and open forum discussions in the investment department to review investment strategy. The asset allocation does not remain static; it is always under scrutiny.

3.5 To Analyse Global Macro Economic Trends

The remit of the committee is to analyse the global macroeconomic trends (the big picture or top-down view) and establish a long-term investment strategy. The shorter-term outlook is also analysed closely, particularly technical and sentiment indicators, in order to take advantage of short-term trading opportunities. Discussions are centred on The Five Tools of Investment.

3.6 Inter-Market Analysis

The committee draws upon the views of all the investment managers in order to arrive at a detailed and formalized top-down view. This has the effect of harmonizing the asset allocation process of Asset Management Service, as it creates a common theme for bond, equity, and cash investment within the different sectors, which then feeds into all other investment portfolios. It does not decide on individual fund selection; this being the responsibility of the individual investment managers.

4. The Five Tools of Investment

4.1 Fundamental Analysis

The financial markets are discounting mechanisms, anticipating events that will not take place for several months. Forecasting the markets is, therefore, a two-stage affair. In the first stage, we determine what is going to happen in the future, and in the second, we determine how much of that future has already been discounted (i.e., factored in) by the financial markets. The first tool, namely Fundamental Analysis, is the first stage of this process. The other four tools constitute the second stage.

Fundamental Analysis involves the study of a range of indicators to determine the outlook for economic growth and inflation – the two principal factors that drive the financial markets. Some of the key variables that we follow are capacity utilization, interest rates, liquidity, currency movements, and commodity prices (particularly the oil price).

4.2 Valuation Analysis

Saying that an asset is expensive is akin to saying that it is priced for perfection. In other words, an asset that is expensive has already discounted all the good news, and its price is likely to fall almost irrespective of what happens in the future. The question is: how do we determine when any particular asset is expensive? The value inherent in bonds is determined by comparing their yields to a number of yardsticks, including current inflation, our in-house estimate of inflationary expectations, and real short-term interest rates. The process for equities is a little more complex and involves regressing historical P/E (price-earnings) ratios against a number of key variables, including bond yields, inflation, and the slope of the yield curve. Valuation Analysis has less relevance for currencies, at least over the short to medium term, but we monitor various measures of purchasing power parity (including the Economist magazine’s Big Mac Index) to identify when a currency is significantly out of line with its true value.

4.3 Sentiment Analysis

Markets tend to bottom when all the news is bad and most investors are negative. There is logic behind this apparently perverse behaviour. When most investors are negative, the likelihood is that everyone who wants to sell has already done so. This means that when the first opportunistic buyers start to buy, there is a dearth of supply, and the investment’s price can rise quite sharply. It is therefore important to keep an eye out for those situations when investors become too negative or too optimistic. There are several ways in which this is done. Firstly, we monitor sentiment surveys that tell us precisely what percentage of investors interviewed expressed a positive view towards a given investment. Secondly, we monitor the commitment of traders' reports to see how speculators are positioned in the futures markets. Thirdly, we assess the consensus view simply by listening to the views being expressed by analysts and by observing the headlines in the financial press.

4.4 Technical Analysis

There are many who believe that the only way to forecast the markets is to analyse their behaviour in the past. Although we are not quite as fanatical about technical analysis as some, we do believe that it plays an important role both in terms of identifying buy and sell opportunities as well as fine-tuning the timing of investment decisions. As far as our top-down strategy is concerned, we prefer to buy on dips and to sell into strength, and hence we employ technical analysis techniques that are consistent with this approach!

4.5 Inter-Market Analysis

There are many different types of analysis that come under this one heading. It can involve comparing current market trends with historical experience or perhaps comparing the performance of different asset classes to see if they are behaving in a consistent manner. Examples in the past have included using previous bubble patterns to forecast the NASDAQ and monitoring the close relationship between bond yields and commodities to confirm what is really happening in the real economy.

5. Investment Process

5.1 Manager Selection

5.1.1 Database Screening

A shortlist of funds is established from all the available collective investment funds. The screening consists of a detailed quantitative risk and return analysis and comparison against peers and benchmarks in order to establish a comprehensive database of the best managers.

5.1.2 Qualitative Assessment and Due Diligence

The process of selecting appropriate fund managers for multi-managers requires not only performance and other quantitative measures, but also knowledge of items that, by their very nature, are subjective and hence require a different form of assessment. It is important to understand the investment manager’s philosophy. An in-depth look at the portfolio manager to indicate his consistency in his specific investment style, investment philosophy, and portfolio management is important to determine if they are true to their stated objective.

The final selection consists of discussions with the key decision-makers, analysis of the company structure, investment process, quantitative aspects, understanding the manager's competitive advantage, examining the manager’s risk management and control procedures, and understanding the portfolios available.

In the case of selecting a hedge fund manager, it is necessary to analyze the candidates in detail, not just from an external perspective (past returns, offering memorandum, etc.), but from an internal viewpoint (investment process and philosophy, style, approach, risk control, performance record against the appropriate index, in various markets and against its peers, depth and quality of internal organization, manager background, investment references, etc.). We look at four key areas in the due diligence process of hedge funds.

- Strategy

It is firstly important that we understand the current investment strategy that a specific fund uses; it is further important to know the following points relating to the strategy:

- Has the fund manager changed his strategy over time?

- Is the current manager responsible for the fund's long-term performance, or did he inherit it?

- Are there limits to the amounts the funds can manage effectively without sacrificing performance with the current strategy?

- Are audited statements available?

- What is the average leverage used?

- How liquid are the positions in the fund?

- The Fund Itself

Attention should be paid to understanding the terms of the fund and its structures, as well as the quality of the various parties involved. We will, in particular, look at the following areas:

- What is the legal structure of the fund (Is it a variable rate debenture structure or a limited partnership, for instance)?

- Is the management firm regulated by the FSB with a Category II A license?

- What is the subscription and redemption policy of the fund?

- What are the fees and expenses charged to the fund and to the investor?

- Who are the fund's service providers (custodian, administrator, accountant, attorney)? It is important that these service providers are independent third parties, and to contact them independently to confirm that they know the manager and that they are not aware of any inconsistencies in the manager’s performances or accounting methods.

- Where are the assets of the fund held? And who has access to the accounts of the funds and what process must be followed to transfer assets?

- What is the process to be followed to value investments, and is it an independent third party that calculates the net asset value of the fund?

- How many other investors are in the fund, how large is the largest investor, and how much of the equity capital was committed by the manager?

- Do any other investors in the fund have preferential terms regarding fees, liquidity, or transparency?

- The Management Team

It is important to know the key individuals of the fund, their backgrounds, and their reputation within the industry, as well as where they gained their experience in managing funds.

- The Investment Process of the Hedge Fund

It is crucial to understand the process of making investment decisions and whether it is an investment committee or a single individual who makes these decisions. We also try to establish if they are allowed to make trades and what assets can be traded. Most funds’ mandates also limit the amount of risk they can take in the portfolio, and it is important to know and understand these imposed limits. Inquiring if the fund has a risk committee and who does the compliance to ensure that the fund stays within its risk limits is essential.

5.2 Risk Control and Portfolio Monitoring

Risk control is an important part of the Kanaan Trust methodology. Not only does it ensure that our investors can sleep at night, but it also helps to prevent unpleasant surprises.

Through the multi-manager approach, the risk profile of the investment portfolio is significantly reduced, as it is not fully exposed to any one underperforming manager or from a change of ownership or key personnel. Managers are selected based on their individual investment style. The combination of managers with different investment styles ensures that investors are never underexposed to a style that is in favor. This approach produces more consistent returns with lower volatility than single manager portfolios through all types of market environments.

Because we invest in a broad array of different asset classes, portfolios benefit from proper diversification.

We believe that risk must be managed proactively rather than reactively. Portfolio monitoring is an ongoing process, both quantitatively and qualitatively, to ensure that the portfolios are managed in accordance with the objective. If the performance of a specific manager is not competitive, the manager will be replaced.

Finally, by its very nature, our approach tends to mean that our many investors are protected against volatility. We aim to be in the right fund at the right time.

6. Restrictions

One of the main advantages of the Kanaan Trust Fund of Funds is that it has very few restrictions when it comes to the investment options available. Whereas a regular equity type unit trust is usually limited to a specific asset class or sector of the market, the Kanaan Trust Funds have a completely flexible asset allocation mandate.

Except for our Kanaan Active Wrap 4 wrap fund, all our other wrap funds can move freely from being 100% invested in equities to being 100% invested in interest-bearing instruments such as Money Market funds. As our Kanaan Active 4 accommodates Retirement Annuities and other Risk Averse Profiles, it can allocate only up to 30% in locally registered offshore funds and must always have a minimum of 25% in conservative funds like the Money Market or Income Funds.

7. Benchmarks

The main benchmark and return objective of the Kanaan Trust Funds is to beat inflation by at least 3%. It, therefore, has an absolute real return objective and will only earn performance fees once this objective has been reached.

When doing peer-to-peer comparison, the following should be noted:

Although Kanaan obtained its Fund Management licenses during 1995, and performed well by switching to cash two weeks before the 1998 Far East Pacific Crash, a few days after the IT Bubble Crash of 2000, and weeks before the 2008 Credit Crunch Crash, Kanaan has decided to close down all its fund of funds as the markets have become increasingly complex after the Credit Crunch Crash. This was when the traditionally free market governments decided to intervene by bailing out many big companies that should have gone bankrupt normally and further by decreasing interest rates and making cash available so as to protect their markets. These interventions have disrupted the normal approximately ten-year growth cycle of the free markets, making it much more difficult to time the big share market crashes.

Kanaan Asset Managers have therefore decided to follow a more conservative strategy by managing many smaller Wrap Funds according to clients' specific risk profiles and circumstances, which would make it impossible to do peer-to-peer comparisons.

8. Disadvantages of Fund of Funds

8.1 As mentioned previously, the benefits of funds of funds for voluntary contributions, where capital gains do not have to be declared every year, have not been weighing up against the disadvantages after the Credit Crunch Crash of 2008. It became increasingly difficult to time the big share market crashes and important, to rather manage clients' funds according to their risk profiles and circumstances, individually through a larger number of affordable smaller cost-efficient wrap funds, where the DFA (Discretionary Financial Advisor) is allowed to manage wrap funds smaller than R50 million, which is the minimum, to be cost-efficient in the case of a fund of fund.

8.2 An accumulation of regulations, as mentioned elsewhere, especially in the case of Hedge Fund of Funds, caused administration costs to increase to such an extent that funds of funds worth less than R50 million could no longer be managed cost-efficiently. As a result, we closed our fund of funds and subsequently moved the compulsory contribution funds to our South African wrap funds. The voluntary contribution funds, as far as possible, were transferred to our offshore fund of funds, hedge fund of funds and funds in Mauritius, where you do not have to declare capital gains once a year. Due to fewer regulations in Mauritius, it is more efficient to manage the funds via fund of funds and funds there.

9. Financial advice

We are contrarian in many aspects as far as financial advice is concerned, regarding where you should save, how much life cover you should take out, how you should structure it, etc. See more about our contrarian methodology under home, professional advice.

9.1 Immediate Capital Planning

We are financial advisers here as well. We advise that one should take out the necessary amount of life cover as soon as possible. In other words, one should not work towards it; you should take it out as soon as possible and reduce it thereafter from time to time as your capital in terms of voluntary contributions and compulsory contributions increase. We advise against life and disability cover that increase year after year with inflation as the premium will increase even faster. We are often criticized for advising that clients should put more emphasis on saving for retirement capital than for life cover and disability cover. We believe that clients should have enough capital at retirement from which they can draw an income equal to their salaries and further, the capital should be enough to allow them to increase their income annually with inflation, without digging into their capital. We do not believe that it is okay for clients to dig into their capital until it becomes zero over the period of their statistical life expectancy. There’s a possibility that clients will live longer and we have found since 1983, that it is very negative for clients to see how their capital reduces year after year.

9.2 Emphasis on Buildup of Retirement Capital

We put a bigger emphasis on the buildup of retirement capital than on life cover, as there is a possibility that a person may not die or become disabled before retirement and if they save too much towards cover, they will have less of their disposable savings available for the buildup of retirement capital. We have seen that by following a macro top-down fund of fund investment strategy, which has given a far above average market-related growth rate, it has allowed us to calculate much less initial life cover for clients, which in turn allows the clients to save much more towards investments, which compounds the end results of investors who are following our contrarian advice. The difference is not big, it is enormous over a period of plus-minus 40 years up until retirement. A young mining engineer who started to follow our advice at age 20, 40 years ago, will have ± R45,000,000 available in retirement capital, compared to his colleague who followed conventional advice with ± R15,000,000.

9.3 Retirement Capital Planning

We are innovative as far as retirement capital and tax planning are concerned and do not mind going contrary to conventional wisdom. This is an area where we are so contrarian that we are criticized by our opposition as controversial and unethical. We do have the necessary qualifications in law, accounting, and mathematics among ourselves and if the numbers show us that the amount of tax the average client will save by contributing towards a retirement annuity or a pension fund, does not weigh up mathematically against the reduced returns of compulsory contribution funds, compared to voluntary contribution funds and the amount of tax the client will pay on income from these compulsory contribution funds one day when he goes on pension, we do not hesitate to advise against retirement annuities and other compulsory contribution funds. Clients who know how to use an ordinary pocket calculator usually follow our advice. We do not say our advice is better or that other advice is wrong. Each client is unique and we acknowledge the fact that a client’s risk profile may require different advice from the mentioned mathematical equations.

9.4 Hedge Funds

Most institutions and financial advisors, as well as economists, emphasize the importance of the diversification of investment portfolios, and we underwrite that importance. However, there is a problem. If you diversify your assets to 8 of the main popular asset classes, you will mathematically dilute your returns. But it is a well-known fact that if the main asset class, alternative assets, is part of the mix, you can get away with diversifying to only 5 main asset classes, namely:

- Equities – e.g., shares, unit trusts, etc.

- Alternative assets – e.g., hedge funds, gold coins, antique cars, etc.

- Property

- Cash – e.g., Money Market, government and industrial bonds, etc.

- Offshore assets

The further problem is that hedge funds, which are a fantastic alternative asset class, are not correlated at all with the other main asset classes. They have not been used by the institutions and financial advisors for the man in the street, only for high net worth individuals. Here we are especially contrarian, as we are, according to our knowledge, the only boutique asset manager who has set up a hedge fund of funds since 2005 with only a minimum investment of R100,000 for the man in the street. As hedge funds are perceived to be only for rich people, the minimum, with all the other funds, is R1,000,000, and that minimum was enforced by the regulator since 1 April 2015. You will notice on the graph of the factsheet (F9) that the dark blue line, which represents Kanaan Hedge FoF, didn’t crash at all like the JSE during 2008. It outperforms the JSE hands down since 2005 with a CAR of 16.24%.

The abovementioned concerning our South African Hedge Funds is now history and something of the past, as mentioned previously, as we have decided to move our voluntary contribution funds, including those invested in hedge funds, to Mauritius where we have much less regulation and worldwide access to much better hedge funds which are dollar denominated.